for Chartered Accountants")

Multi-disciplinary Partnerships (MDP) under the Chartered Accountants Act, 1949: Comprehensive Briefing

Executive Summary

To address the increasing complexity of global business, technology, and financial reporting, the Institute of Chartered Accountants of India (ICAI) has established guidelines for the formation of Multi-disciplinary Partnerships (MDPs). Effective July 8, 2021, these guidelines allow Chartered Accountants in practice to partner with specific non-CA professionals to provide a holistic “complete package of services.”

The core takeaways are as follows:

- Purpose: To enhance audit quality and professional agility by integrating specialists in areas such as data analytics, blockchain, and industry-specific expertise.

- Permitted Partners: Partnerships are restricted to members of specific professional bodies, including Company Secretaries, Cost Accountants, Engineers, Architects, and certain Actuaries. Notably, partnerships with Advocates are currently barred due to existing Bar Council of India rules.

- Regulatory Compliance: MDPs must be registered with the ICAI, adhere to strict naming conventions (including an “MDP” suffix), and undergo mandatory KYC verification for non-CA partners.

- Statutory Audit Limitations: Under the Companies Act, 2013, an MDP can only perform statutory audits if a majority of its partners (calculated by both headcount and profit share) are Chartered Accountants.

- Disciplinary Oversight: Professional misconduct remains the jurisdiction of the respective professional bodies governing each partner.

1. Rationale for Multi-disciplinary Partnerships

The business environment has undergone a significant transformation characterized by complex supply chains, cross-border transactions, and sophisticated financial instruments. This evolution has necessitated a shift in the audit profession:

- Complexity of Financial Reporting: Accounting standards and industry-specific rules often require specialized expertise beyond traditional accounting.

- Technological Integration: The rise of data analytics, blockchain, and artificial intelligence requires the audit profession to be agile and employ diverse skilled professionals.

- Integrated Thinking: A multi-disciplinary approach combines deep assurance methodologies with subject-matter expertise, meeting the modern expectations of stakeholders and society.

- Global Alignment: The MDP model aligns with professional structures already adopted in jurisdictions such as the United Kingdom, Germany, and Australia.

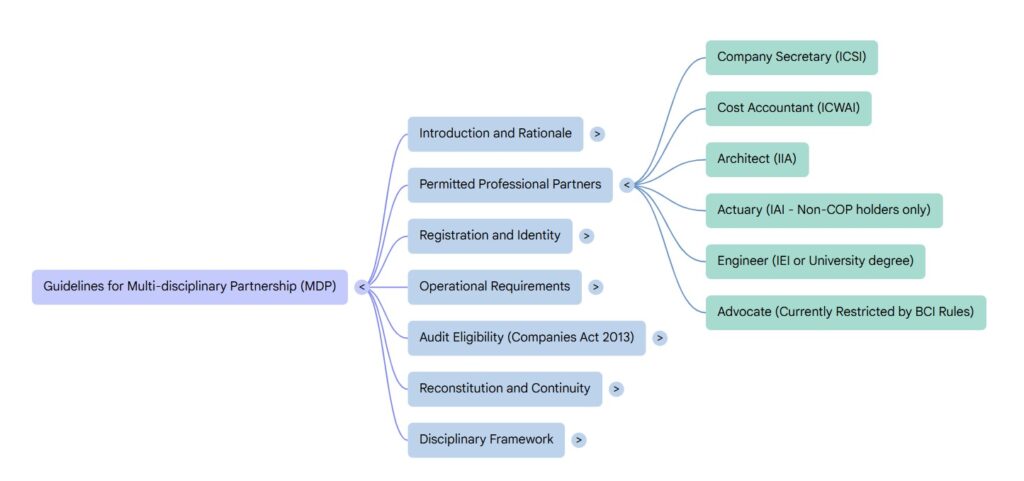

2. Permitted and Restricted Professional Partnerships

Under Regulation 53B, Chartered Accountants are permitted to enter into partnerships with specific recognized professions. However, the legal feasibility of these partnerships often depends on the regulations of the partner’s respective professional body.

Permitted Partners

| Professional Category | Governing Body/Act | Feasibility Status |

| Company Secretary | The Institute of Company Secretaries of India (ICSI) | Permitted; ICSI regulations allow for such partnerships. |

| Cost Accountant | The Institute of Cost and Works Accountants of India (ICWAI) | Permitted; ICWAI regulations allow for such partnerships. |

| Engineer | The Institution of Engineers / Recognized Universities | Permitted; must be an elected member or hold a degree from a university established by law. |

| Architect | The Indian Institute of Architects | Permitted; must be a registered member. |

| Actuary | The Institute of Actuaries of India | Conditional; Permitted only if the Actuary does not hold a certificate of practice. |

Prohibited or Restricted Partners

- Advocates: While Regulation 53B lists Advocates, the Bar Council of India Rules, 1975 currently prohibit advocates from entering into partnerships or sharing remuneration with non-advocates. Consequently, MDPs cannot include Advocates until these rules are amended.

- Actuaries with CoP: MDPs are not permitted to enter into partnership with a member of the Institute of Actuaries of India who holds a certificate of practice.

- Other Exclusions: Currently, individuals with postgraduate qualifications in management, approved valuers, insolvency professionals, and IT professionals are not permitted to be admitted as partners in an MDP CA firm.

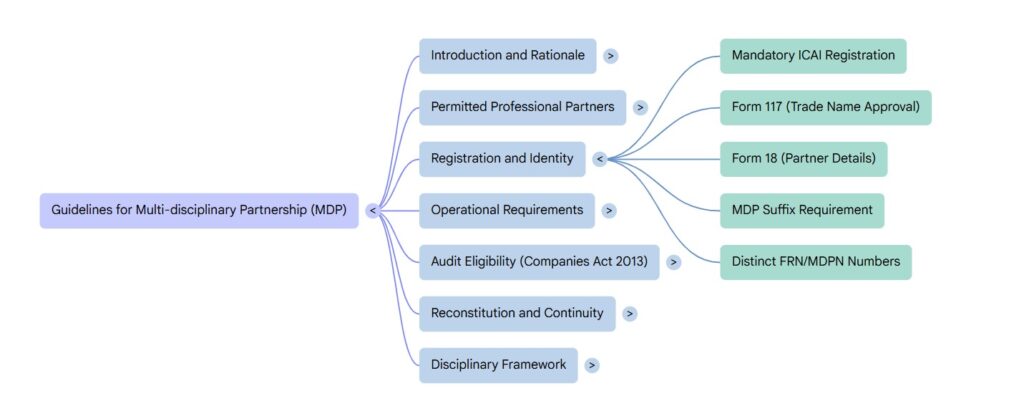

3. Constitutional and Registration Framework

MDPs can be established as either traditional partnership firms under the Indian Partnership Act, 1932 or as Limited Liability Partnerships (LLPs) under the Limited Liability Partnership Act, 2008.

Registration Process

- Trade Name Approval: New firms must apply to the Council using Form 117 for trade name approval.

- Constitution/Admission: Existing firms admitting non-CA partners or new firms must submit details via Form 18 within 30 days of the change.

- Naming Conventions: To distinguish MDPs from traditional CA firms, they must include a mandatory second line: “Multi-disciplinary Partnership of Chartered Accountants” or “MDP of Chartered Accountants.”

- Registration Numbers: The registration number will include the abbreviation “MDP” (e.g., MDP000001W) to differentiate it from standard Firm Registration Numbers (FRN).

Verification and KYC

- Documentary evidence for non-CA partners (membership certificates or degrees) must be attested by a practicing Chartered Accountant not related to the firm.

- The Head Incharge of the MDP is responsible for submitting annual KYC documents for all non-CA partners.

4. Operational Guidelines and Audit Eligibility

Statutory Audit under the Companies Act, 2013

Eligibility for appointment as a statutory auditor is strictly governed by the “Majority Criteria.” An MDP is eligible only if:

- The majority of partners are Chartered Accountants.

- Calculation: This majority is determined by both the number of partners and their aggregate share of profits.

- Signing Authority: Only partners who are Chartered Accountants are authorized to act and sign on behalf of the firm in audit matters.

- Ceiling Limits: For computing audit ceiling limits, only practicing CA partners are considered.

Administration and Management

- Profit Sharing: The MDP has the discretion to decide profit-sharing ratios among partners.

- Branch Offices: Per Section 27 of the Act, branch offices must be in the charge of a Chartered Accountant. While the Council can grant exemptions to allow a non-CA partner to lead a branch, this requires a specific request.

- Partner Restrictions: A non-CA professional cannot be a partner in more than one MDP of CAs. Furthermore, the Head Incharge of an MDP cannot be a partner in any other MDP registered with different professional bodies.

5. Reconstitution and Disciplinary Oversight

Continuity of MDP Status

If all non-CA partners leave the firm, the MDP has a 60-day window to admit new non-CA professionals. Failure to do so results in:

- The automatic closure of the MDP; or

- Conversion of the MDP back into a standard CA firm, requiring the removal of the MDP designation from its name.

Disciplinary Proceedings

Misconduct is handled according to the laws governing the individual partner’s profession:

- Chartered Accountants: Subject to the Chartered Accountants Act, 1949.

- Cost Accountants: Subject to the Cost and Works Accountants Act, 1959.

- Company Secretaries: Subject to the Company Secretaries Act, 1980.

- Architects: Subject to the Architects Act, 1972.

- Actuaries: Subject to the Actuaries Act, 2006.

- Engineers: Subject to the general principles of civil law.

Beyond the Balance Sheet: The Strategic Rise of Multi-disciplinary Partnerships

1. The Hook: The End of the Silo

The modern business landscape is no longer defined by simple ledgers or local commerce. Today’s organizations navigate a volatile web of global supply chains, decentralized blockchain transactions, and intricate cross-border ownership structures. In this high-stakes environment, the traditional “siloed” approach to professional services is reaching its limit. A single discipline can no longer provide the comprehensive oversight or agility required to audit a multi-national entity. The solution is the Multi-disciplinary Partnership (MDP)—a strategic evolution that allows Chartered Accountants (CAs) to collaborate across professional boundaries to meet the needs of an increasingly complex global economy. For firms that fail to adapt, the risk is not just a lack of growth, but eventual obsolescence.

2. Takeaway 1: It’s No Longer Just About the Numbers

The role of the auditor is shifting from narrow financial verification toward “integrated thinking.” To maintain quality in an era of data analytics and artificial intelligence, the profession must embrace a diverse skill base. Modern financial reports are often governed by specialized industry rules that require technical expertise beyond the traditional scope of accounting.

By partnering with architects, engineers, and actuaries, CAs ensure that an audit reflects both the physical reality of assets and the mathematical modeling of future risks. This collaborative model is the most effective mechanism for developing the expertise needed for quality assurance in specialized businesses.

“A multi-disciplinary approach, drawing on deep methodology and frameworks for assurance, combined with specialist and subject matter expertise, possess the bandwidth to meet this need and will be increasingly vital as the market continues to evolve towards integrated thinking in the years to come.”

3. Takeaway 2: The “Advocate” Paradox (The Legal Red Tape)

While Regulation 53B of the Chartered Accountants Regulations permits CAs to form partnerships with Advocates, there is a significant regulatory hurdle that acts as a veto. This “Advocate Paradox” arises because the Bar Council of India (BCI) Rules do not currently mirror the flexibility found in the CA Act.

Specifically, Rule 2 of Chapter III of Part IV of the Bar Council of India Rules, 1975, strictly prohibits an Advocate from entering into a partnership or sharing remuneration with any person who is not an Advocate.

Warning: Until the Bar Council of India amends its internal rules, MDPs cannot legally include practicing Advocates as partners. For the strategy-minded practitioner, this is a “trap for the unwary” where permission from one professional body is neutralized by the restrictions of another.

4. Takeaway 3: The Power of the Majority (Statutory Audit Limits)

For firms aiming to provide statutory audits under the Companies Act 2013, the composition of the partnership is strictly governed by Section 141. Eligibility to be appointed as a company auditor is not granted to every MDP; it is reserved for those where the “core” remains firmly under the control of CAs. To meet the “Majority Criteria,” the firm must satisfy two distinct requirements:

- Headcount: The majority of the total number of partners must be Chartered Accountants.

- Profit Share: The aggregate share of profits in the MDP must be held by the Chartered Accountant partners.

Key Insight: This dual requirement functions as a regulatory safeguard. It ensures that even in a diverse, multi-disciplinary environment, the professional liability, assurance integrity, and the authority to sign financial statements remain with qualified CAs.

5. Takeaway 4: Identity is Mandatory (The Naming Convention)

Transparency is the cornerstone of the MDP framework. The Institute mandates specific branding to ensure that stakeholders can distinguish an MDP from a traditional CA firm at a glance. Every MDP must include a mandatory descriptive second line and an updated registration number that supplements the existing Firm Registration Number (FRN).

MDP Branding Standards: ABC & Co Multi-disciplinary Partnership of Chartered Accountants FRN: 123456W MDPN: MDP000001W

Strategic Note on Operations: Under Section 27 of the Act, only a CA may be in charge of a branch office. However, the Council may grant exemptions to allow a non-CA partner to lead a branch. Furthermore, firm leaders should note that risk management remains fragmented: in the event of misconduct, each partner remains subject to the disciplinary proceedings of their own respective professional Act (e.g., the Architects Act, 1972 or the CS Act, 1980).

6. Takeaway 5: The Actuary Restriction

The rules regarding partnership with Actuaries contain a nuance that often surprises firms looking to scale insurance or pension advisory arms. While CAs can partner with members of the Institute of Actuaries of India, the partnership is only permitted if the Actuary does not hold a Certificate of Practice (CoP).

If an Actuary holds a valid CoP, the partnership is strictly barred. This restriction is rooted in the Actuaries Act, 2006, which deems it professional misconduct for a practicing actuary to share profits with non-actuaries. This creates a strategic hurdle for firms seeking to integrate top-tier practicing actuarial talent into their partnership structure.

7. Conclusion: The Agile Auditor

The shift toward Multi-disciplinary Partnerships represents a fundamental move toward agility. By breaking down the walls between accounting, engineering, and actuarial science, firms can finally provide the holistic insights that modern stakeholders demand.

As technology like AI and blockchain becomes standard, the “traditional” single-discipline firm faces a vital question: will it remain relevant, or will it eventually become a relic of a simpler past? The future belongs to those who can integrate diverse expertise into a single, cohesive framework of quality assurance.

The ability to draw on a diverse skill base is no longer a luxury; it is a vital necessity for providing quality assurance in a complex global economy.

Connect with CA Devesh Thakur

Stay updated with structured Income Tax learning, section-wise breakdowns, practical insights, and regular tax updates across platforms: