TDS Journal Entries – Clear, Practical Explanation

Most people learn TDS entries by memorizing formats. That approach fails in real work. If you don’t understand the logic behind the entry, you will misstate liabilities, expenses, or both.

This guide explains TDS from the ground level and then connects each journal entry with accounting rules, purpose, and financial impact.

What is TDS?

TDS (Tax Deducted at Source) is a system where tax is collected at the time of payment.

When certain payments are made—salary, rent, professional fees, contractor payments—the payer deducts a percentage and deposits it with the government.

The payer is not the taxpayer. The payer is only collecting tax on behalf of the government.

Example:

Professional fee = ₹1,00,000

TDS @10% = ₹10,000

You pay:

- ₹90,000 to the professional

- ₹10,000 to the government

Total expense remains ₹1,00,000.

Accounting Foundation You Must Remember

Before posting TDS entries, recall the Golden Rules:

Personal Account

Debit the receiver, Credit the giver

Real Account

Debit what comes in, Credit what goes out

Nominal Account

Debit all expenses and losses, Credit all incomes and gains

TDS entries follow these rules consistently.

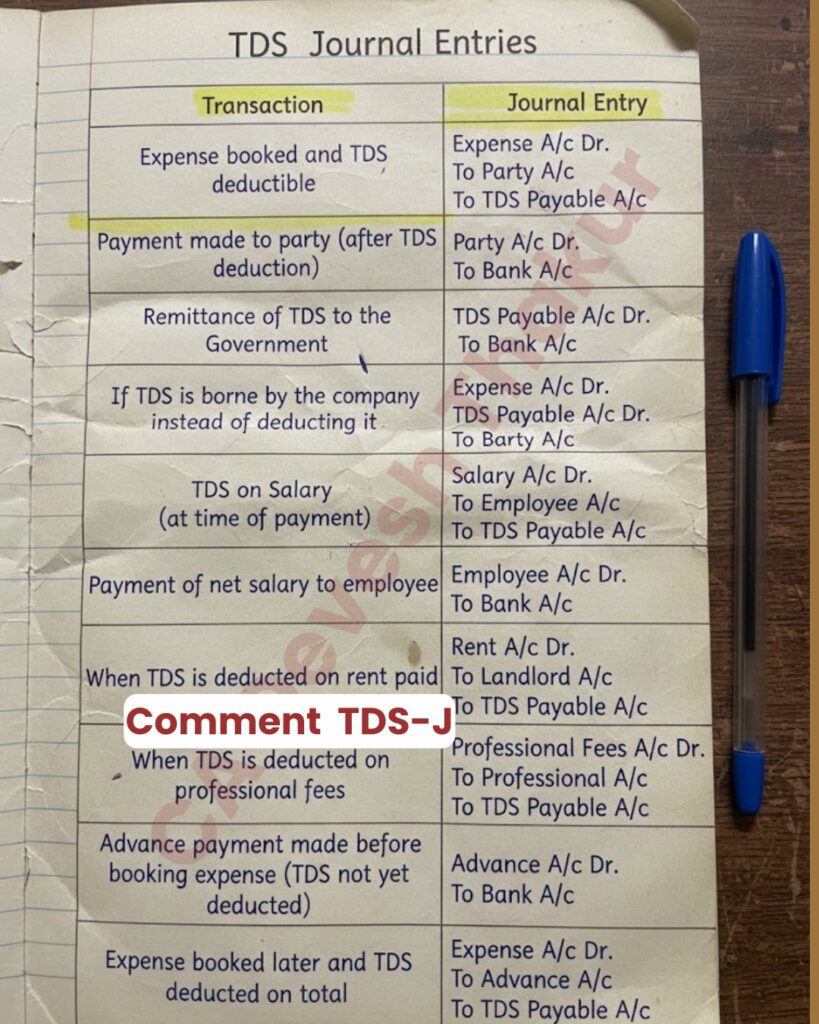

1. Expense Booked and TDS Deductible

Entry

Expense A/c Dr

To Party A/c

To TDS Payable A/c

Why this structure?

- Expense is a Nominal Account → Debit

- Party is a Personal Account → Credit

- TDS Payable is a liability → Credit

You incurred the full expense. You now owe:

- Net amount to the party

- Tax amount to the government

Effect on Financial Statements

Profit & Loss Account

Expense increases by full amount.

Balance Sheet

- Creditor (net amount)

- TDS Payable (liability)

The expense is always recorded at the gross amount, not net of TDS.

2. Payment to Party (After TDS Deduction)

Entry

Party A/c Dr

To Bank A/c

You are settling the payable.

- Party is Personal → Debit

- Bank is Real → Credit

Impact

Balance Sheet

- Bank decreases

- Creditor reduces

No effect on P&L.

3. Remittance of TDS to Government

Entry

TDS Payable A/c Dr

To Bank A/c

- TDS Payable is liability → Debit to remove

- Bank → Credit

Impact

Balance Sheet

- Bank decreases

- TDS liability cleared

No P&L impact.

4. When Company Bears TDS (Grossing Up Case)

In some agreements, the recipient must receive a fixed net amount. The company pays TDS in addition.

Example:

Professional must receive ₹1,00,000 net.

TDS @10%

Gross amount becomes ₹1,11,111

TDS = ₹11,111

Entry

Expense A/c Dr 1,11,111

To Party A/c 1,00,000

To TDS Payable A/c 11,111

Here, tax becomes additional cost.

Impact

P&L

Expense increases by gross amount.

Balance Sheet

- Party payable (net agreed amount)

- TDS payable

This is the only case where TDS increases expense.

5. TDS on Salary

At the time of salary booking:

Salary A/c Dr

To Employee A/c

To TDS Payable A/c

- Salary → Nominal → Debit

- Employee → Personal → Credit

- TDS Payable → Liability → Credit

Payment of Net Salary

Employee A/c Dr

To Bank A/c

Employee liability settled.

TDS will later be deposited using:

TDS Payable A/c Dr

To Bank A/c

6. TDS on Rent

Rent A/c Dr

To Landlord A/c

To TDS Payable A/c

Rent is expense.

Landlord is creditor.

TDS payable is liability.

Structure remains identical.

7. TDS on Professional Fees

Professional Fees A/c Dr

To Professional A/c

To TDS Payable A/c

Same accounting logic. Only account name changes.

8. Advance Payment Before Expense Booking (No TDS Yet)

If advance is paid before expense recognition:

Advance A/c Dr

To Bank A/c

Expense is not yet incurred, so no TDS at this stage (unless specifically required under law at payment stage).

Impact

Balance Sheet

- Advance becomes asset

- Bank decreases

No P&L effect.

9. Expense Booked Later and TDS Deducted

When expense is finally booked:

Expense A/c Dr

To Advance A/c

To TDS Payable A/c

- Expense recognized

- Advance adjusted

- TDS liability created

Overall Flow of a TDS Transaction

Every TDS transaction usually moves through three stages:

- Expense booking → Liability created

- Payment to party → Creditor cleared

- Payment to government → TDS liability cleared

If any stage is skipped in books, reconciliation will fail.

Financial Impact Summary

| Stage | P&L Impact | Balance Sheet Impact |

| Expense booking | Expense increases | Creditor + TDS liability created |

| Payment to party | No impact | Bank ↓, Creditor ↓ |

| TDS deposit | No impact | Bank ↓, TDS liability ↓ |

Key Clarity Points

- TDS is not your expense.

- TDS is not your income.

- You are a collector for the government.

- Only when tax is borne by you does it increase expense.

- Always record expense at gross amount.

")

{kind=link}