CA Devesh Thakur

CA Devesh Thakur

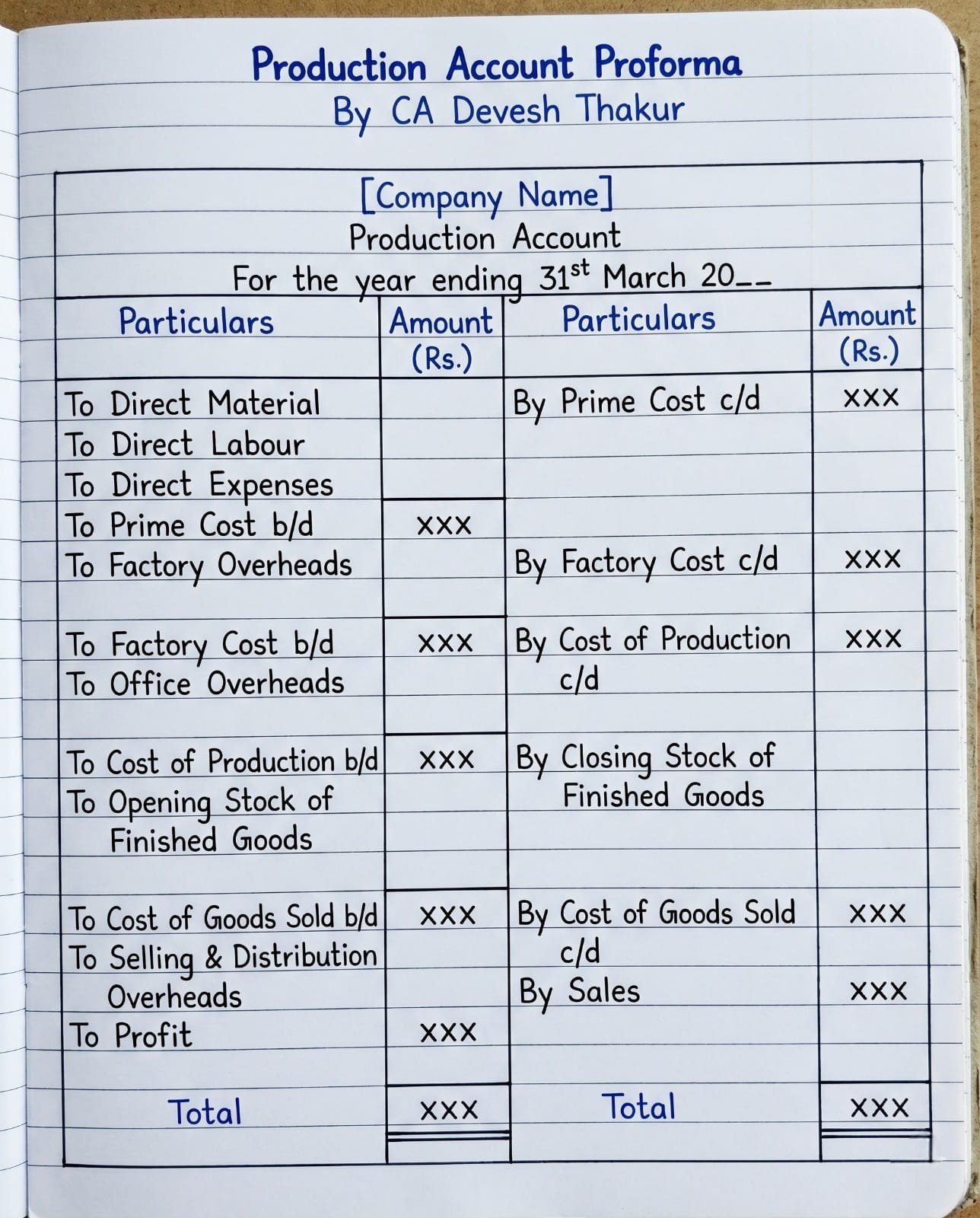

A Production Account is a statement prepared by manufacturing businesses to ascertain the Cost of Production of goods manufactured during a specific period. It records all expenses incurred in converting raw materials into finished goods and helps management determine manufacturing efficiency and production costs.

1. Output Costing

Method to determine the cost per unit of production.

Example: Total Cost ₹1,00,000 ÷ 10,000 Units = ₹10/unit

2. Cost Sheet

Statement showing total cost and cost per unit.

- Cost Control

- Price Fixation

- Profit Planning

- Decision Making

3. Prime Cost

All direct costs related to production.

Example: ₹50,000 + ₹20,000 + ₹10,000 = ₹80,000

4. Factory Cost (Works Cost)

Prime Cost plus indirect factory expenses.

- Factory Rent & Electricity

- Supervisor Salary

- Machine Repairs

5. Cost of Production

Total cost incurred till goods are manufactured.

6. Cost of Sales

Total cost incurred to sell goods including selling & distribution overheads.

- Advertisement

- Sales Commission

- Delivery / Freight

7. Work-in-Progress (WIP)

Partially completed goods not yet ready for sale.

Example: Car assembly started but incomplete.

8. Finished Goods

Fully completed products ready for sale.

- Ready furniture

- Ready garments

- Ready mobile phones

9. Scrap

Residual material left after the production process.

- Iron Pieces

- Wood Dust

- Plastic Waste

Prime Cost

| Particulars | Amount |

|---|---|

| Direct Material | xxx |

| Direct Labour | xxx |

| Direct Expenses | xxx |

| Prime Cost c/d | xxx |

Factory Cost (Works Cost)

| Particulars | Amount |

|---|---|

| Prime Cost b/d | xxx |

| Factory Overheads | xxx |

| Factory Cost c/d | xxx |

Cost of Production

| Particulars | Amount |

|---|---|

| Factory Cost b/d | xxx |

| Office & Admin Overheads | xxx |

| Cost of Production c/d | xxx |

Cost of Goods Sold (COGS)

| Particulars | Amount |

|---|---|

| Cost of Production b/d | xxx |

| + Opening Stock of Finished Goods | xxx |

| − Closing Stock of Finished Goods | (xxx) |

| Cost of Goods Sold c/d | xxx |

Cost of Sales & Profit

| Particulars | Amount |

|---|---|

| Cost of Goods Sold b/d | xxx |

| Selling & Distribution Overheads | xxx |

| Profit | xxx |

| Sales | xxx |

| Cost Stage | Formula |

|---|---|

| Prime Cost | Direct Material + Direct Labour + Direct Expenses |

| Factory Cost | Prime Cost + Factory Overheads |

| Cost of Production | Factory Cost + Office Overheads |

| Cost of Goods Sold | Cost of Production + Opening FG − Closing FG |

| Cost of Sales | Cost of Goods Sold + Selling & Distribution Overheads |

| Profit | Sales − Cost of Sales |

📦 Raw Material

Starting point of production

🟠 Prime Cost

DM + DL + DE

🔵 Factory Cost

Prime Cost + Factory OH

🟣 Cost of Production

Factory Cost + Office OH

🟡 Cost of Goods Sold

COP + Opening FG − Closing FG

🟢 Cost of Sales

COGS + Selling OH

💰 Profit / Loss

Final outcome

- Production Account helps manufacturing businesses find the total cost of production

- Prime Cost = Direct Material + Direct Labour + Direct Expenses — the foundation

- Factory Cost adds indirect factory expenses (rent, electricity, repairs) to Prime Cost

- Cost of Production further adds office & administrative overheads

- COGS adjusts for opening and closing finished goods stock

- Profit = Sales − Cost of Sales (after adding selling & distribution overheads)

- WIP = partially done goods; Finished Goods = ready for sale; Scrap = production waste

⚡ Student Shortcut — Remember This!

🔒 Get Your Free Study Notes

Follow CA Devesh Thakur on Instagram to unlock the free download of Production Account Complete Notes.