Section 82: Capital Gain Exemption

Complete guide to Section 82 of the Income Tax Act, 2025 (Old Section 54) — Capital Gain Exemption on Sale of Residential House. Flowcharts, case laws, CGAS rules, ₹10 Cr cap, two-house option & the RLITAS framework — decoded simply.

Note includes watermark. Comment ‘Capital Gain’ on Instagram to get full notes.

Section 82 Capital Gain – CA Devesh Thakur

📲 Follow @cadeveshthakur.official for daily Income Tax updates!

1. Core Concept — Understand This First

When an individual or HUF sells a residential house property and earns Long-Term Capital Gain (LTCG), the government allows exemption if that gain is reinvested into another residential house.

👉 That’s the entire intent.

Everything else = conditions, limits, and traps.

Section 82 of the Income Tax Act, 2025 is simply a restatement of the old Section 54 — with better structure and clarity. No conceptual change. Only clarity improvement.

2. Applicability Conditions — Foundation Layer

All of the following conditions must be met simultaneously. If even ONE fails — no exemption.

Type of Assessee

Only Individual or HUF. Companies, firms, LLPs, etc. are not eligible under Section 82.

Asset Sold

Must be a Residential House Property. Agricultural land, commercial property, or other assets don’t qualify here.

LTCG Required

The gain must be Long-Term Capital Gain. Short-term capital gain on the old property = no Section 82 exemption.

Investment in New House

Must invest in a New Residential House in India. Foreign property does not qualify.

Time Limits

Purchase: 1 year before or 2 years after sale. Construction: 3 years after sale.

Lock-in Period

New house must not be sold within 3 years of purchase/completion. Otherwise cost adjustment applies.

❌ If even ONE condition fails → No exemption

This is non-negotiable. Students and professionals often try to argue partial compliance — the law does not permit it.

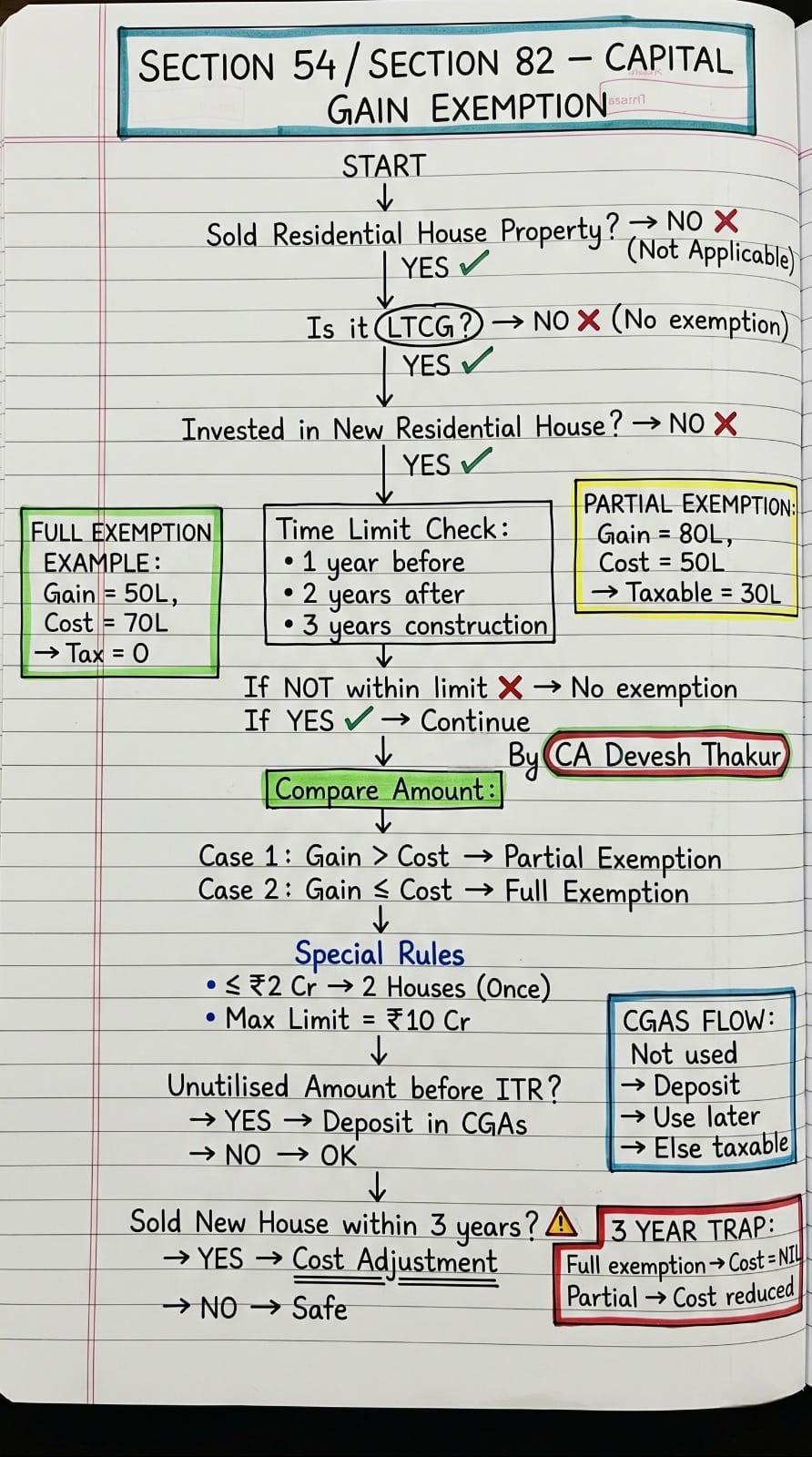

3. Complete Decision Flowchart

4. Exemption Logic — Full vs Partial

The amount of exemption under Section 82 depends on a direct comparison between the Capital Gain earned and the Cost of the New House purchased.

Cost ≥ Gain → Full gain is exempt

Cost < Gain → Only cost amount is exempt

📌 The Simple Formula

Exemption = Lower of (Capital Gain, Cost of New House)

Subject to the ₹10 Crore cap (Section 7 below).

5. Most Ignored Rule — Sale Within 3 Years

If the new house is sold within 3 years of purchase or construction, the exemption already claimed is clawed back via a cost adjustment rule. This is where students lose marks and professionals make costly mistakes.

Entire sale proceeds become taxable as STCG!

Cost = Original Cost − Exemption Claimed

🔑 Key Takeaway

The cost of the new house is reduced by the exemption amount if sold within 3 years. This inflates the capital gain on the new house’s sale — effectively reversing the earlier exemption.

6. Capital Gain Account Scheme (CGAS)

If the capital gain is earned but not fully utilised before the due date of filing ITR, the taxpayer must deposit the unutilised amount in a Capital Gain Account Scheme (CGAS) with an authorised bank to preserve the exemption.

💡 Common Mistake

Many people think they can simply wait to buy the house. Wrong. If you don’t deposit unutilised gains in CGAS before ITR due date, the exemption is forfeited for that amount — even if you later buy the house within the time limit.

7. Special Provisions

Two House Option

If Capital Gain is ≤ ₹2 Crore, the taxpayer can invest in two houses (instead of one). This option is available only once in a lifetime. Cannot be exercised again in future years.

₹10 Crore Cap

Even if you invest more, maximum exemption is capped at ₹10 Crore. Example: Gain = ₹20 Cr, Investment = ₹20 Cr → Exemption = ₹10 Cr only. Remaining ₹10 Cr is taxable.

8. Section 54 vs Section 82 — Real Difference

| Parameter | Section 54 (Old ITA 1961) | Section 82 (New ITA 2025) |

|---|---|---|

| Assessee | Individual / HUF | Individual / HUF Same |

| Asset Type | Residential House | Residential House Same |

| Gain Type | LTCG | LTCG Same |

| Time Limits | 1 yr before / 2 yrs / 3 yrs | 1 yr before / 2 yrs / 3 yrs Same |

| ₹10 Cr Cap | Yes (introduced via amendment) | Yes — explicitly stated Clearer |

| 2 House Option | Yes (once, ≤₹2 Cr gain) | Yes — explicitly stated Clearer |

| CGAS | Required | Required Same |

| Core Concept | 👉 No conceptual change. Only clarity improvement. | |

9. Important Judicial Decisions — Simplified

Most blogs dump case names without meaning. Here’s what actually matters for each decision:

10. Common Mistakes — Reality Check

Let’s be blunt — students and even professionals mess these up regularly:

👉 Key Insight

If you’re making these mistakes, you don’t understand the section — you’re just memorising it. Understanding the intent (why the exemption exists) prevents 90% of errors.

11. Memory Framework — RLITAS Rule

A simple, effective, exam-proof checklist. Before claiming Section 82 exemption, run through each letter:

📌 RLITAS — Simple, Effective, Exam-Proof

Run through this before every Section 82 problem in exam or practice. If any letter fails, there is no exemption or the exemption is limited.

Comment ‘Capital Gain’ on Instagram to get the full Section 82 notes. Follow @cadeveshthakur.official.

12. Final Conclusion

Section 82 (Income Tax Act, 2025) is not a new concept — it is a refined, structured version of the old Section 54 with explicit language and better clarity.

✔ The Real Challenge

The real challenge is not understanding the law — it’s applying it correctly under pressure (exam or real case).

If you:

- Follow the flow (use RLITAS)

- Understand the logic (not just memorise)

- Remember the traps (CGAS, 3-year rule, ₹10 Cr cap)

You won’t just pass exams — you’ll avoid costly tax mistakes in real life.

This is exactly what CA Devesh Thakur teaches across all platforms — not just section names and conditions, but the why behind every rule.

💬 Get Full Notes

Comment ‘Capital Gain’ on the Instagram reel to receive complete Section 82 handwritten notes. Follow @cadeveshthakur.official on Instagram so you never miss an update from the Income Tax Act 2025 Series!

📥 Section 82 Notes

📌 How to save on mobile:

iOS: Long-press image → “Save to Photos”

Android: Long-press image → “Download image”

© CA Devesh Thakur | eTaxSave.com

{kind=link}