Author: CA Devesh Thakur

Category: GST Basics | 30 Days GST Challenge – Day 5

Introduction

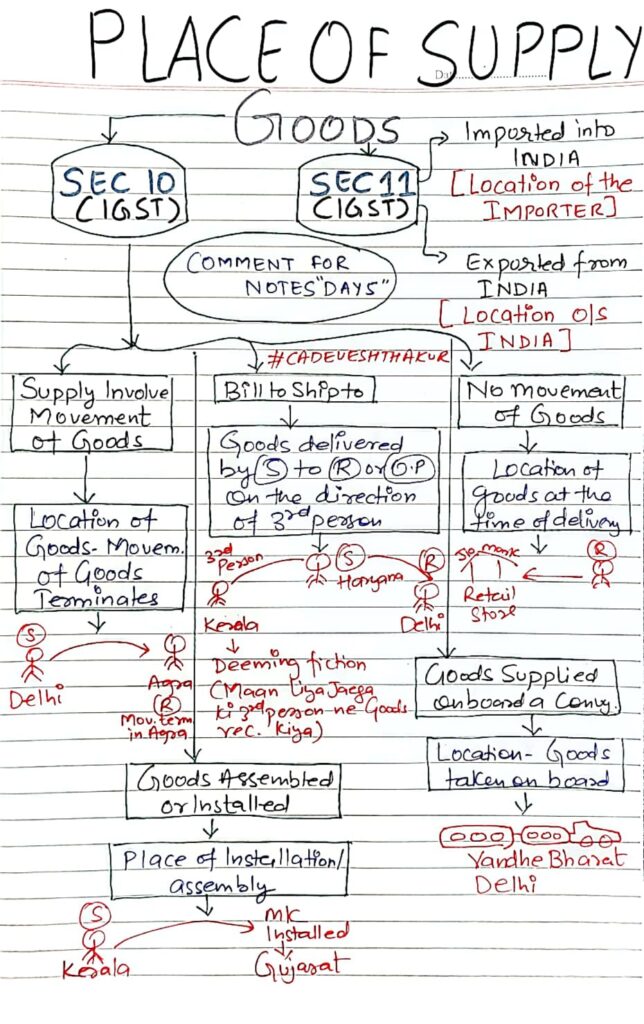

The concept of Place of Supply plays a crucial role in determining whether a supply is inter-state or intra-state, which further affects whether IGST or CGST & SGST will be levied. For goods, this is governed by Sections 10 and 11 of the IGST Act.

Let’s decode these sections with practical illustrations.

Applicable Provisions: Sec 10 & Sec 11 of IGST Act

Section 10 – When the supply of goods is within India

This section applies when both supplier and recipient are located in India.

Section 11 – When the supply of goods involves import/export

This section deals with supplies where either the supplier or recipient is located outside India.

Section 10 – Detailed Scenarios and Examples

Movement of Goods by Supplier, Recipient or Other Person

Provision:

If the supply involves movement of goods (by the supplier, recipient, or any other person), the place of supply is the location where movement terminates for delivery.

Example:

- Supplier (S) in Delhi sends goods to recipient (R) in Agra.

- Movement terminates in Agra.

Place of Supply: Agra (Uttar Pradesh)

Inter-State Supply – IGST Applicable

“Bill To – Ship To” Scenario

Provision:

When goods are delivered by the supplier to a third person on the direction of the buyer (deemed recipient), the place of supply is the location of the person who gave the direction.

Example:

- Buyer (3rd Person) in Kerala instructs Seller (S) in Haryana to deliver goods directly to another recipient (R) in Delhi.

- Though goods are delivered to Delhi, they are billed to Kerala.

Place of Supply: Kerala

Deemed that 3rd person has received the goods

No Movement of Goods

Provision:

When there is no movement of goods, the place of supply is the location of the goods at the time of delivery.

Example:

- Goods picked up by buyer from a retail store in Delhi.

Place of Supply: Delhi

Intra-State Supply – CGST + SGST Applicable

Goods Installed or Assembled at Site

Provision:

If goods are supplied and are to be installed or assembled at a site, the place of supply is the place of installation/assembly.

Example:

- Machinery sent from Kerala and installed in Gujarat.

Place of Supply: Gujarat

Tax determined based on location of installation

Goods Supplied on Board a Conveyance

Provision:

Where goods are supplied on board a conveyance (e.g. train, aircraft, vessel), the place of supply is the location at which such goods are taken on board.

Example:

- Goods supplied on Vande Bharat train while boarding in Delhi.

Place of Supply: Delhi

Section 11 – Import and Export of Goods

Goods Imported into India

Provision:

Place of supply for imports is the location of the importer.

Example:

- Goods imported by a company in Mumbai.

Place of Supply: Mumbai

Goods Exported from India

Provision:

Place of supply for exports is outside India, but for GST compliance, it is deemed to be the location outside India.

Example:

- Goods exported from Delhi to the USA.

Place of Supply: USA (outside India)

Export – Zero-Rated Supply

Summary

| Scenario | Section | Place of Supply | Example |

| Movement of goods | Sec 10 | Place where movement terminates | Delhi → Agra → Agra |

| Bill to – Ship to | Sec 10 | Location of the person who ordered | Kerala orders, ship to Delhi → Kerala |

| No movement of goods | Sec 10 | Location at time of delivery | Picked from Delhi retail store → Delhi |

| Goods installed/assembled | Sec 10 | Place of installation/assembly | Installed in Gujarat → Gujarat |

| Supplied on a conveyance | Sec 10 | Location where goods taken on board | Vande Bharat, boarded in Delhi → Delhi |

| Import of goods | Sec 11 | Location of importer | Importer in Mumbai → Mumbai |

| Export of goods | Sec 11 | Outside India | Export to USA → Outside India |

Conclusion

Understanding the Place of Supply is key to determining the correct GST liability. Whether you’re a trader, manufacturer, or a service provider dealing in goods, a correct classification under Section 10 or 11 of the IGST Act can ensure compliance and smooth business operations.

Connect with CA Devesh Thakur

Stay updated with structured Income Tax learning, section-wise breakdowns, practical insights, and regular tax updates across platforms:

{kind=link}